Melbourne Residential Market: Signs of a Structural Turning Point

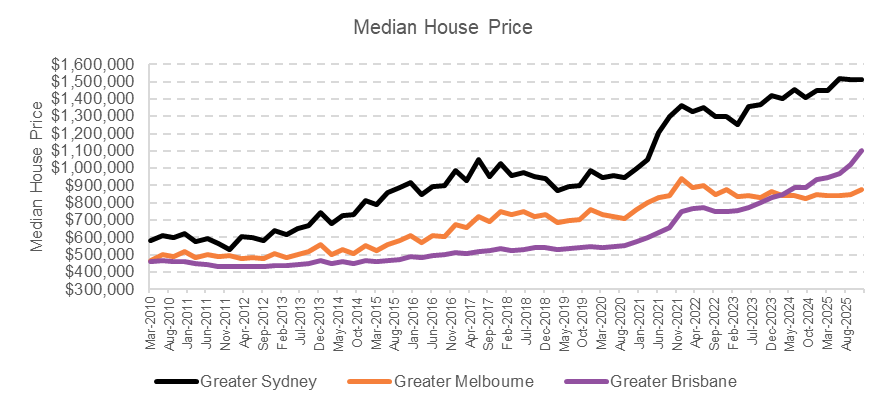

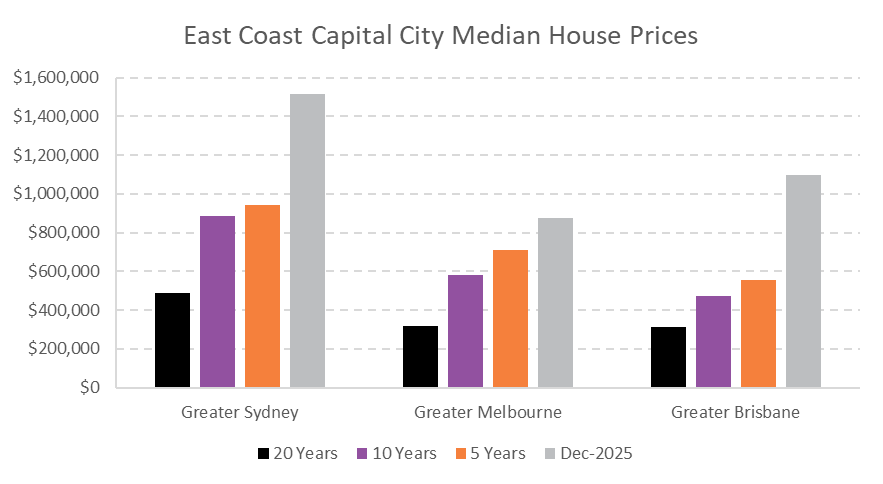

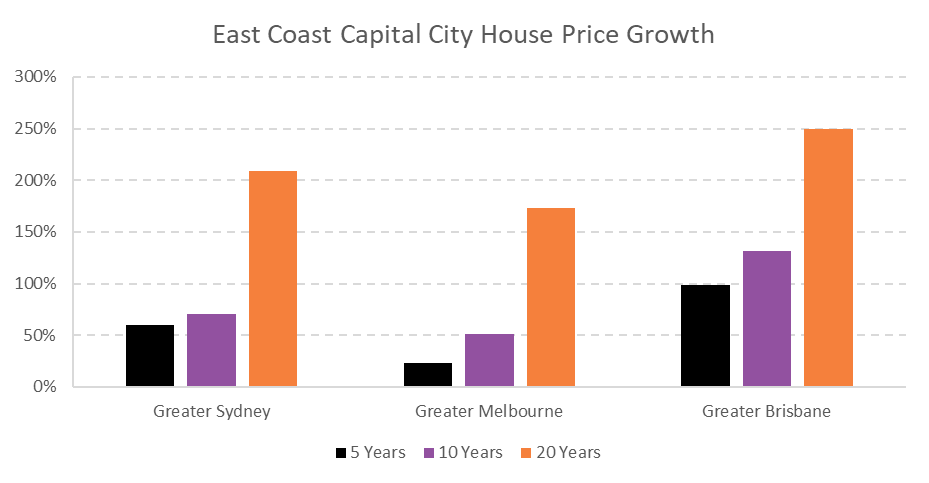

Since late 2021, Melbourne’s residential housing market has undergone a sustained period of value erosion relative to Australia’s other major capital cities. What was historically the nation’s second most expensive residential market has, over the past several years, experienced a notable shift in both price performance and population dynamics.

A key driver of this change has been migration. During the post-pandemic period, Victoria recorded significant net interstate migration losses, with a large share of departing residents relocating to Queensland. This population movement, combined with rising interest rates and elevated housing supply, contributed to a prolonged softening in Melbourne’s housing values whilst contributing to Brisbane’s.

The shift has been sufficiently pronounced that by March 2024 Brisbane overtook Melbourne in median house prices, a reversal of long-standing market hierarchy. Current data indicates that Brisbane now holds an approximate $225,000 premium in median house prices relative to Melbourne—a development that would have been difficult to envisage several years ago.

However, the structural dynamics underpinning Melbourne’s housing market now appear to be changing.

As Melbourne’s relative affordability widened compared with both Sydney and Brisbane, the financial rationale for interstate relocation has weakened. Selling property in Melbourne at a relative discount only to purchase into increasingly expensive markets has become less economically attractive for many households. This shift has already begun to moderate the pace of interstate migration out of Victoria, with net migration flows moving toward equilibrium. It is likely that as Melbourne’s economy recovers, younger people will be drawn to Melbourne.

At the same time, international migration has accelerated strongly, restoring a key pillar of housing demand for the Melbourne market. Population growth is once again contributing meaningfully to underlying demand for both rental and owner-occupied housing.

Throughout 2023 and early 2024, market conditions remained firmly in favour of buyers, largely due to a significant pipeline of development stock—largely across all sectors, though particularly pronounced in broad hectare land holdings. However, this surplus supply is unlikely to persist over the short to medium term. Rising construction costs, financing constraints, and developer risk aversion have curtailed new project commencements across Victoria. As a result, existing stock is expected to be progressively absorbed as population growth and confidence strengthens. The market will turn quickly to one of FOMO as new stages will see costs to produce lots increase.

Policy settings are also becoming more supportive of the residential sector. Government incentives and grants aimed at stimulating residential construction and facilitating first-home buyer participation are beginning to influence activity levels. In parallel, the likelihood of further monetary tightening is contributing to improved market confidence with regard to locking in interest rates and stabilising borrowing capacity.

Taken together, these factors suggest Melbourne may be approaching the early stages of a cyclical inflection point. Relative affordability compared with Sydney and Brisbane, stabilising migration flows, strengthening population growth, and a constrained future development pipeline collectively create conditions conducive to renewed price momentum.

From a strategic perspective, Melbourne’s current position presents a potentially attractive entry point within the national housing cycle. For both investors seeking value relative to other capital markets and owner-occupiers prioritising long-term fundamentals, Melbourne may increasingly represent one of the more compelling residential opportunities in Australia over the next phase of the cycle.

In summary, while the past several years have seen Melbourne underperform relative to its interstate counterparts, the underlying fundamentals are now realigning in a manner that suggests the market may be turning the corner. For stakeholders with a medium-to-long-term investment horizon, Melbourne’s residential market warrants renewed strategic attention.

Matthew Gross | Director | mgross@nprco.com.au

Nicholas Price | Associate Director | nprice@nprco.com.au