Generational blame solves nothing

There is a lot of discussion at present around affordability, taxation treatment of residential assets and generational wealth gaps. Whilst there are some merits of truth to many of the arguments, sometimes you just can’t change the demographic profiles of society as it ages and the influences that have occurred, particularly post 1985 when the Australian Labor Party introduced the Capital Gains Tax and the current form of Negative Gearing in 1987. What most won’t know is that negative gearing has been in Australia’s taxation system since 1936. When the ALP stopped Negative Gearing in 1985, the shortage of housing was so bad that they reinstated it two years later as rents spiked significantly. Unless the Government is prepared to take up the slack by Mum and Dad investors leaving the housing market, they may well want to think through thoroughly how they would fund the shortfall and whether it would genuinely impact house prices in a meaningful way. In fact there was no meaningful house price correction or change in values in 1985-1987.

If the government thinks it can rectify the housing market through death duties, then it is misleading the public and fattening its own coffers after running years and years of budget deficits. This will not address the issues of trade shortages and premiums attached to this lack of investment, expensive supply chains, low productivity, planning geared to the higher costs of multi-storey density (but cheaper for councils, not the consumer), extraordinary immigration rates compared to historical norms, cost of buying a site and the time it takes to gain an approval – often a minimum of a decade for master planned communities etc.

However, you can’t get away from demographic transition. The Baby Boomers are the wealthiest generation to date, having achieved this through hard work and simply getting old. As Baby Boomers reach end of life, they will logically pass on their wealth to the next generation as will Generation X to Millennials/Generation Y and on it goes.

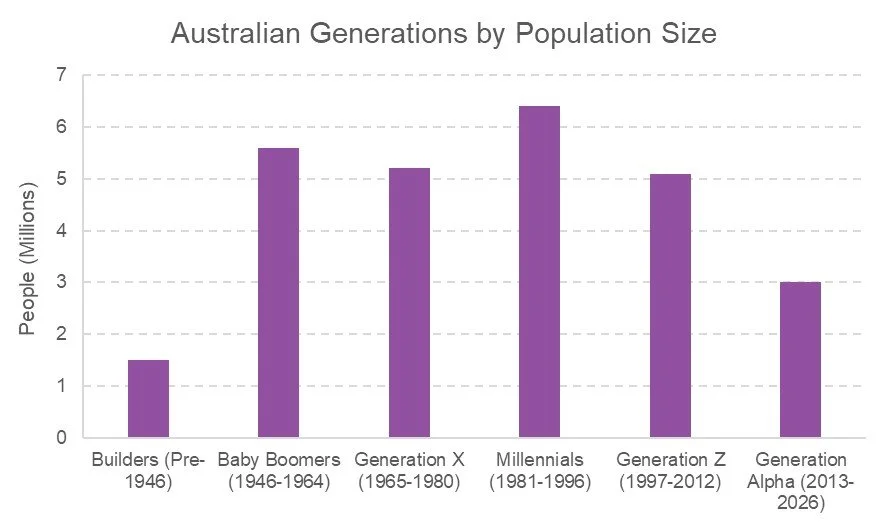

So with the finger squarely pointed at the two generations often maligned for ruining affordability for younger generations, a quick snapshot of “Boomers” and “Gen X” is called for. As an aside, the Millennials/Generation Y are now the biggest voting cohort in Australia. This is a generation that is moving forward rapidly into property and possibly the most at risk of structural reform and price moderation.

Baby Boomers (Born 1946–1964)

Age in 2026: 62–80 | Life Stage: Retirement & Transition

Wealth Profile

Baby Boomers remain Australia’s wealth anchor. This generation holds the largest share of household net wealth, largely driven by long-term residential property appreciation and equity market exposure. It is very difficult to beat time in market whilst also acknowledging that many of the houses owned by this demographic which were once on the urban fringe are now inner to middle ring suburbs. By default, these are typically the most expensive properties. They didn’t design this economic outcome, time and population growth did it for them.

Typical wealth composition includes:

· Mortgage-free principal residence

· Investment property holdings (though on a per capita basis, less than Generation X)

· Superannuation (often in pension phase and not for their whole working life)

· Direct shares and cash deposits

Superannuation Characteristics

Compulsory superannuation began in 1992, meaning earlier Baby Boomers had limited early-career exposure. Younger Boomers benefited from compounding contributions and rising Superannuation Guarantee rates. Many now draw income via account-based pensions and utilise downsizing strategies to boost balances. By default, this often frees up larger dwellings for families creating a more economical use of Australia’s housing stock. If you were to remove the Boomers wealth; taxes would be significantly higher to fund a grossly larger government sponsored pension. This would impact significantly every trailing generation thereafter.

Property Ownership

Baby Boomers dominate outright home ownership statistics. Many hold significant housing equity and some investment property exposure. Australia is entering a major intergenerational wealth transfer phase as this cohort transitions capital to younger generations. You can’t escape generational shifts.

Generation X (Born 1965–1980)

Age in 2026: 46–61 | Life Stage: Peak Earnings & Wealth Accumulation

Wealth Profile

Generation X represents Australia’s primary accumulation cohort. Now in peak earning years, many rely on dual-income households and maintain higher mortgage leverage than Baby Boomers did at comparable ages.

Common wealth characteristics:

· Primary residence with significant mortgage balance (though usually much less than those entering the market today if buying like for like)

· Exposure to investment property (which has been enhanced by greater financial awareness and increased capabilities that technology has created in sourcing property compared to the previous generation that relied on the Saturday Paper’s Real Estate section)

· Growing superannuation balances (often with housing exposure because of a lifetime of superannuation contributions and trusting property as a more reliable asset class less impacted by changes the Federal Government makes to superannuation)

· Participation in equities and managed funds

Superannuation Characteristics

Generation X is the first cohort with near full-career exposure to compulsory superannuation. Contribution rates have increased over time, and many members engage actively with diversified investment strategies, including self-managed super funds (SMSFs) which often choose residential property as part of their portfolio.

Property Ownership

Home ownership remains strong among Generation X, though affordability pressures were more acute at entry compared to Boomers. This cohort is highly sensitive to interest rate cycles and employment stability at the end of the cohort, less so at the beginning as retirement is nearing.

Strategic Outlook

Over the coming decades, Baby Boomers will progressively draw down superannuation and release housing equity. Generation X will simultaneously accumulate wealth while inheriting intergenerational capital. Together, these two cohorts anchor the majority of Australia’s household balance sheet and will shape fiscal, housing, and retirement policy outcomes. How the current and successive government’s treat this accumulation of wealth will have very significant impacts on future generations.

Whilst there is no doubt that intergenerational equality in wealth has arguably never been more stretched, it is hardly the fault of the generations that played by the rules set by the government and policy makers at all levels of government. A repurposing of wealth within the private sector is a far better outcome than a repurposing of wealth into the public sector. Future generations that can pay for their own retirement will make it far easier for those generation that would otherwise have to fund it.

One thing that must be remembered is that it took many decades to get to this point, it will not be unwound in a couple of years. Knee jerk policies today whilst sometimes short sighted and well intentioned can have enduring legacies…just look at our regional plans, lack of investment in trades and immigration numbers as an example.

Matthew Gross | Director | mgross@nprco.com.au

Nick Price | Associate Director | nprice@nprco.com.au