If Apartment Values Fall, So Will Housing ... Simultaneously

There has been so much speculation around the apartment market and how it could impact the broader housing sector, however history tell us that this hasn't been the case in the past since 2003. The data actually demonstrates that the apartment market and housing market typically move as one, a really important consideration if you believe there will be an uplift or a fall. Often there is the expectation that every cycle is different, but that is hardly the case in property. Developers build too much on the back of confidence, they stop building and the market catches up, reaches equilibrium for a short period of time and then we over build again and hence the cycle starts all over. If it didn't, then the notion of the "property clock" would cease to exist.

The average change from quarter to quarter;

• Detached is 1.2%

• Attached is 1.0%

The worst change from quarter to quarter;

• Detached is -11.1%

• Attached is -4.7%

The greatest positive change from quarter to quarter;

• Detached is 16.0%

• Attached is 8.0%

Sydney has the greatest volatility in the residential market of all the main cities. This volatility is also greatest when consideration is given to apartments and housing as can be seen by the significant swings in the quarterly data above.

The latest ABS data (March 2017) suggests that the detached housing market has experienced a significant correction, however this needs to be treated with caution until further releases can demonstrate this as a real trend or simply a data/market anomaly.

By and large, the two markets move together, albeit housing is the more likely to experience the greatest quarterly correction in Sydney.

The average change from quarter to quarter;

• Detached is 1.3%

• Attached is 1.1%

The worst change from quarter to quarter;

• Detached is -7.4%

• Attached is -4.6%

The greatest positive change from quarter to quarter;

• Detached is 11.6%

• Attached is 8.3%

Melbourne follows a similar trend to Sydney albeit less dynamic. Again, the housing and apartment markets appear to move relatively similarly from one quarter to the next which is as you would expect. However, what most people would think is that the volatility in house prices would be less than the apartment market. This is not the case for Sydney or Melbourne, whilst Brisbane is more evenly matched.

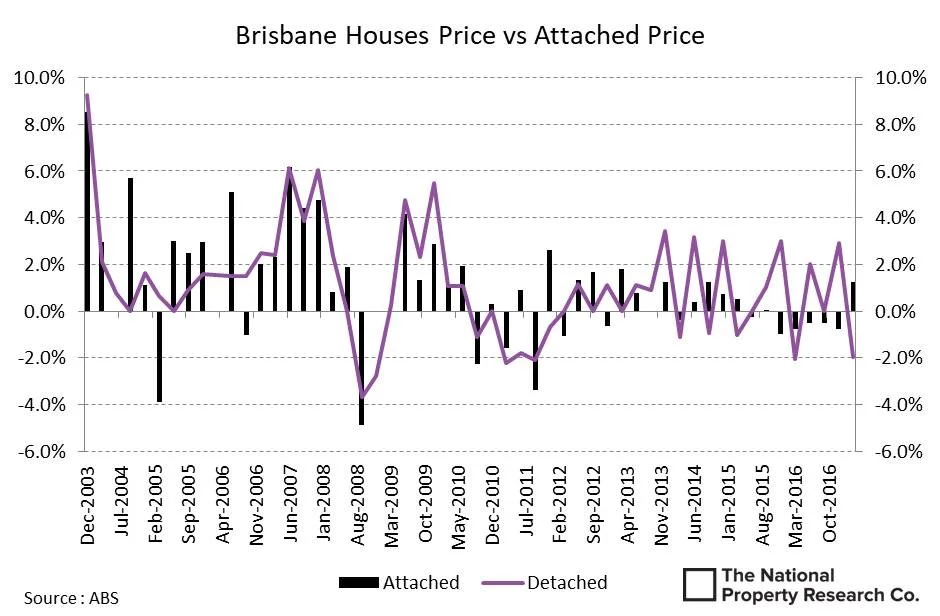

The average change from quarter to quarter;

• Detached is 1.1%

• Attached is 1.1%

The worst change from quarter to quarter;

• Detached is -3.7%

• Attached is -4.9%

The greatest positive change from quarter to quarter;

• Detached is 9.2%

• Attached is 8.5%

Brisbane is unique on the East Coast of Australia in that the market travels more or less in a parallel in terms of quarterly movement. However, when the market softens, it has been the apartment market which has fallen harder than the housing market. Notable periods were March 2005, September 2008 and most recently September 2011. March 2005 represented the start of the next property boom in Brisbane, September 2008 was the GFC and September 2011 was effectively the bottom of the post GFC cycle, though the recovery has been soft compared to Sydney and Melbourne. This largely comes back to lacklustre employment conditions and poor population growth by historical standards, almost the polar opposite of Sydney and Melbourne.

The average change from quarter to quarter;

• Detached is 1.4%

• Attached is 1.4%

The worst change from quarter to quarter;

• Detached is -4.4%

• Attached is -4.5%

The greatest positive change from quarter to quarter;

• Detached is 10.8%

• Attached is 12.2%

Perth is quite similar to Brisbane in that the market again moves quite homogenously. The only real difference being that the negative trends are largely on par, though the positive growth is where apartments actually outperform housing. In this respect, Perth stands alone.

Even with significant economic events as the GFC, the housing and apartment markets have largely moved as one. Speculation around an apartment Armageddon and housing being immune would likely prove to be something not seen before. The other aspect is that downward trends in value of significant substance in any capital city market are generally quite shallow by comparison to the upside. What is more likely to add support to the Apartment market is the various planning policies around the country that are pushing to higher densities closer to the city, thereby fueling demand.

Food for thought.